Introduction to a 529 Plan:

A 529 plan is designed to encourage saving money for future education costs. The tax-advantaged savings plan has two types, including prepaid tuition plans and education savings plans.

Prepaid tuition plans:

A type of 529 plan that lets an account owner purchase units or credits at participating colleges or universities for future tuition for the account beneficiary. One of the main limitations of these plans is the money usually cannot be used to pay for future room and board at universities and colleges. It does not allow the saver to prepay for tuition for elementary, middle or high school.

If the beneficiary does not attend a participating colleges or universities

The prepaid tuition plan may pay less than or even pay a small return on the original investment to the beneficiary. The account owner can also name a new beneficiary from the same family, such as a sibling, or cousin.

Education savings plans:

A type of 529 plan that lets an account owner open an investment account to save for the account beneficiary’s qualified higher education expenses or tuition for elementary or secondary public, private, or religious schools (U.S. Securities and Exchange Commission, 2018). These plans can generally be used at any U.S. university and college, and sometimes certain limited non-U.S. universities and colleges. Individuals can withdrawal up to $10,000 per year per beneficiary for qualifying expenses.

Impacts of 529 plan towards the federal and state income taxes:

| Contributions | Withdrawals |

| May deduct contributions from state income tax or matching grants but may have various restrictions or requirements. | If the withdrawals are for qualified higher education expenses or tuition for elementary or secondary schools, earnings in the 529 account are not subject to federal income tax and, in many cases, state income tax.

However, if 529 account withdrawals are not used for qualified higher education expenses or tuition for elementary or secondary schools, they will be subject to state and federal income taxes and an additional 10% federal tax penalty on earnings (U.S. Securities and Exchange Commission, 2018). |

Impacts of recent tax law changes towards the plan child’s private school education:

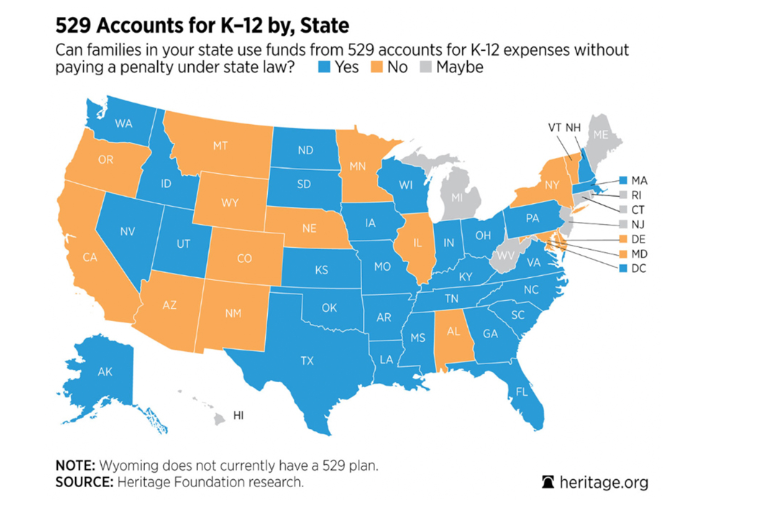

Account owners of the 529 Plans can use their savings for K-12 tuition without penalty for particular states as seen below via the Heritage Foundation research.

Expenses for investing in a 529 Plan:

The following table shows how 529 plan expenses can be spent.

| Prepaid tuition plans | Education Savings Plans |

| · Enrolment/application fees

· Ongoing administrative fees |

· Enrolment/application fees

· Annual account maintenance fees · Ongoing program management fees · Ongoing asset management fees |

Upper limit of the contributions:

The contributions that the account saver make to the qualified tuition program are treated as gifts to the student, but the contributions will generally qualify for the gift tax exclusion amount ($15,000 for 2018, (note this amount may change based on IRS rules). Individuals may be able to contribute more by making certain elections.

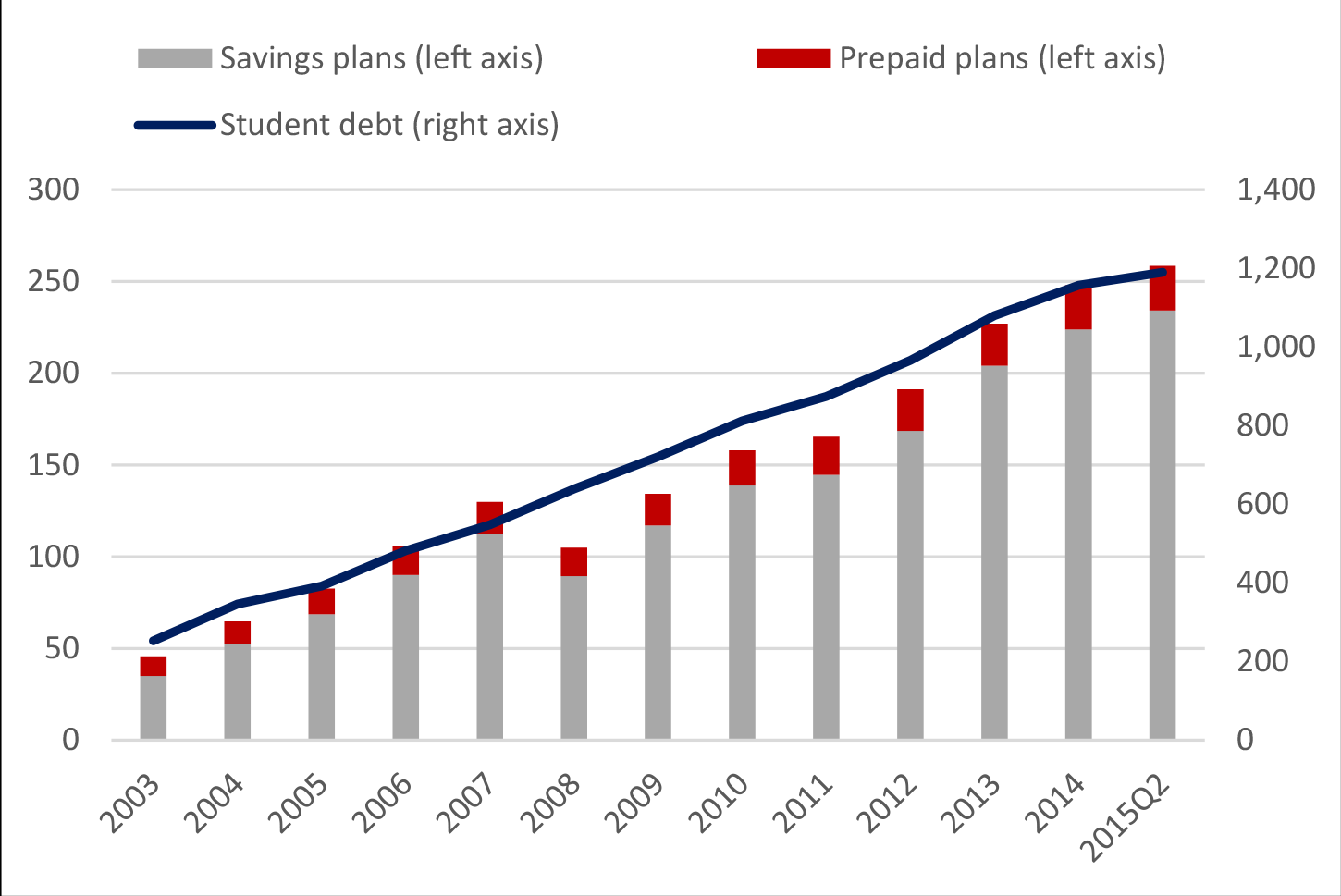

Q: What have been the past growth trends of 529 plans?

A: Based on the federal reserve, the chart below shows that 529 plan assets have generally been growing at the same rate as student loans. The only exception occurred in 2008, when college saving plans’ assets dipped with the market. They lost about 20 percent in value, falling from $113 billion in 2007 to $90 billion in 2008. Prepaid plan assets, which are presumed to represent the size of the state liability, grew smoothly over the period, reaching $24 billion (that is, about 10 percent of total 529 plan assets) in 2015.

Please contact us if you have any tax related questions and we can assist.

Important Notice

The information contained herein serves as a guideline and is only provided for general informational purposes. It should not be considered as offering any tax advice as your situation may differ. Since tax laws are complex, you should consult your tax advisor on specific issues related to your individual tax situation.